This post is about some of the myopic views on disruption in financial services (or any other vertical for that argument), and why I am getting a bit tired of FinTech, RegTech, InsurTech, or whatever AbcTech you may come up with.

Disrupted - Petervan Artwork - Acryl on Paper format A1

Most of the discussions in FinTech are about the (by now outdated) “unbundling” of highly vertical integrated organizations like banks. Everybody recalls the famous CB-Insight slides on how all functions on the website of HSBC, Wells Fargo, or fill in your <Bank Name> here, will be replaced by better offerings of startups or scale-ups: “everything gets fragmented”, you know 😉

It even leads to a “Re-bundling” of financial services, as what was once unbundled needs now to be re-bundled by “banking-as-a-platform” or “Fintegration”, just to throw another buzzword into the mix.

This is in my opinion a highly simplistic view on disruption. It is a fragmented view on disruption. The disruption view is fragmented: each little function on its own is subject of a fragmented disruption debate. We are missing the holistic view of what is going on.

What I would like to bring into the conversation is the “inter-connectedness” of everything, or the “entanglement” of everything.

For payments, the conversation is usually about how many and which intermediaries are part of a payment transaction from the payer to the payee, and how they add value, friction and costs into the system: one can indeed draw disintermediation maps and articulate how the different new entrants attack the different pieces of the end-to-end transaction. But it is piecemealed view, as if the sum of the atomic transactions is an exact equation of the value created in those ecosystem value chains.

The same reflections can be made on the securities business, where many different players (exchanges, central counterparties (CCPs), central securities depositories (CSDs), brokers, custodians and investment managers) are part of the end-to-end flow of atomic transactions between the issuer of a security and the consumer of that security. See also recent comprehensive post by Let’s Talk Payments.

The point I am trying to make here is that what needs to be solved, re-thought and re-designed is a deep ecosystem entanglement. What are really needed are a fundamental process redesign and process innovation and that is not an easy undertaking with all the network effects that are inherent in these ecosystems.

The other point I am trying to make is nobody – not the incumbents, nor the startups/scale-ups – is in a position to solve this on their own.

I believe we have to evolve from platform capitalism to platform cooperation or even platform co-operativism.

- Instead of talking about optimized correspondent banking, the conversation should be one of collaborative/cooperative banking.

- Instead of talking about optimized securities lifecycles and settlement, the conversation should be one of collaborative/cooperative securities markets.

The system is not broken. It works very well for what it was designed for. It does not need to be fixed. It needs to be re-thought. What we are witnessing is the need for a fundamental re-thinking of our assumptions. The financial system is part of a broader system of capitalism based on neoliberalism. That system is broken.

Paul Mason – who wrote the book “Post-Capitalism” – was very clear in his recent keynote to the Glasgow Economic Forum: “Neoliberalism is broken”. And he goes on:

- information technology has paralysed capitalism’s capacity to adapt

- information technology creates a short-cut to abundance

- the root cause of the boom-bust cycles, collapsing productivity, stagnation and policy paralysis is that the markets are sending us a signal that there’s not enough value in a high-tech economy to justify current valuations — of debt, equities or derivatives

- we are in a long transition beyond capitalism, in which the state, the market and a non-market sector based on collaborative production will jostle and coexist

- and that the only theory that can encompass all of these facts is the one originated by the man quoted on the poster behind me [Adam Smith] — a modernised form of the labour theory of value.

That is the first simplification in the current mainstream thinking about disruption.

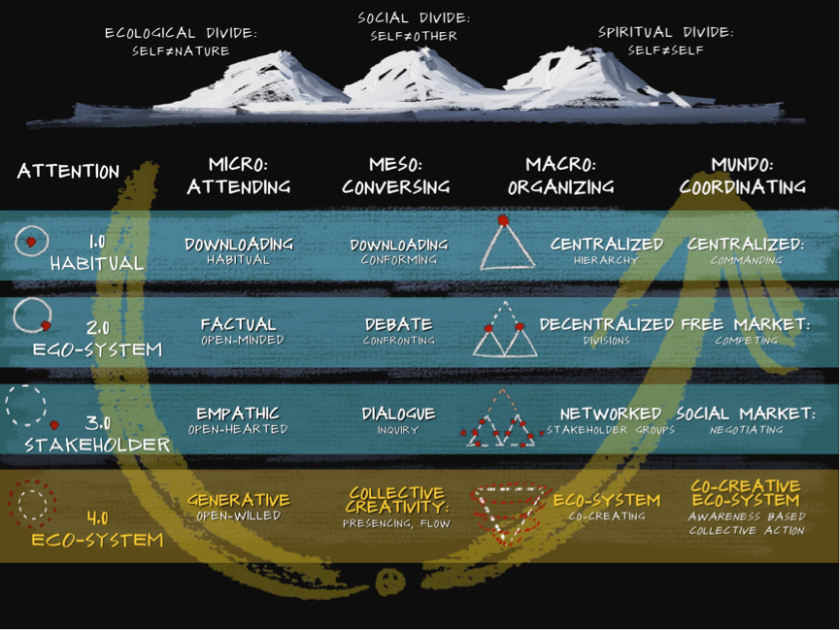

As a start, one should start looking at the symptoms of that broken system (as very well articulated in Otto Scharmer’s work at the MIT U.Lab). These symptoms are:

- An Ecological divide

- A Social divide

- A Spiritual divide

The second simplification of the disruption discourse is the lack of inclusion of the macro-forces. Some of the macro-forces deeply driving what’s going on are:

- Technology macro-force. Here is where inter-connectedness hits hardest. However, this is probably the easiest macro-force to deal with, as technology will take care of itself, as it always has. Open source and other collaborative models will only speed-up that self-care of technology: standards will emerge almost naturally, by natural selection, or my monopolistic interventions.

- Regulatory macro-force. Regulation is still very high on the agenda of financial institutions, and one can only expect that more is to come, especially on the area of data capitalism, handling of personal and corporate data, and even data ethics. After having digested the regulatory impact of the 2008 financial crisis, many are tempted and seduced to jump back with relief into innovation. The blockchain hype is a great excuse for claiming one is busy with the future state of things. Nothing could be further from the truth

- Geo-political macro-force: Grexit, Brexit, Terrorism, War, Surveillance, climate, and other crisis that can pop-up at any moment in time, with their potential of killing overnight all the innovation plans and ambitions.

- Eco macro-force: the acknowledgement that our organizations don’t operate in isolation, that we have to evolve from ego-businesses to eco-businesses, not only extracting value out of the ecosystem for our sole and own benefit, but that we are part of a reciprocal non-zero-sum game with an unspoken desire to save humanity.

The third simplification is the omission of the time component of evolution. I strongly recommend you discovering the work of Simon Wardley and his “situational awareness maps”.

Different values are created by different versions of different technologies and value engines, each of them evolving at their own pace on the lifecycle of emerging to commodity/utility. For big organizations – like financial institutions – it is extremely difficult to map out the current state, let’s not even mention the ability to strategically decide where one wants to head for in different time horizons in the future.

The same situational awareness is not only needed for (existing) and new technologies, but also for existing and new regulations, geo- and eco- events and ambitions.

In the past many have been concerned with the “backward compatibility” of new services and solutions. Backwards compatibility with the existing footprint and practices in the market that is.

I believe there is room today to start thinking in terms of “Forward Compatibility”.

What is Forward Compatibility? It is a capability to plan ahead for gradual adoption by the ecosystem, taking into account the different barriers mentioned above. This is about knowing HOW to get at the new destination:

- How you rally the main stakeholders of the ecosystem into a rigorous system and process innovation? Process innovation is different from process-, datamodel-, or messaging standardization. It is not about standardizing the existing and guaranteeing backwards compatibility with the existing. It is about co-creating a new reality.

- How you promote the evolution from the current model to the future model? In the case of distributed ledger technologies for example, it is not about a tabula rasa that will eradicate the existing, but how one evolves from for example a messaging hub-and-spoke paradigm towards business objects and lifecycles in the cloud, initially probably in one central database (one node), and then evolve to a peer-to-peer networks of many distributed databases or nodes (remember the Digital Asset Grid?)

- How to bootstrap this new reality taking into account the network effects to be created and promoted in the new P2P reality.

No disruption will happen without fundamental re-design – or better re-invention – of the end-to-end business processes:

- Organizations knowing where they want to get and defining and leading that journey;

- De-risking change throughout this journey;

- Making trade-offs in the breadth ànd depth of the destination;

- Moving beyond the atomic nature of the transaction. As mentioned an nausea in previous posts, it is not good enough anymore to enable (atomic) transactions, the challenge is to enable commerce, as an end-to-end process

Startups/Scale-ups who want to be part of this endeavor, will need to know how to “scale”: they will need to learn to appreciate the mechanics of growing a startup into a corporate. This growth process (and its associated growth pains) is very well described in the post “Go Corporate or go home” around the concept of legibility of on organization. The startup organizations – whether they like it or not – will need to become more legible, more predictable. The author makes a very solid argument why hierarchies are needed.

“The smaller a company is, the less they need to formalize anything, and the less the three levels — chain of command, business process, and culture — differ.”

As they grow, they will have to synchronize how they transform these three levels (chain of command, business process, and culture). It’s not only from small self-sufficient team into hierarchies; it is also growing into professional business processes, and evolving the social fabric and conventions.

Although startups, scale-ups, and corporate innovation sandboxes mimicking the startup culture “love to have and keep the flexibility, the cost of growth is scale, integration, and profitability.”

In this context, it is probably worth having a look at the post about the Transferwise culture (I could have taken any other scale-up for that matter) “We inspire smart people and we trust them”, and especially the comment on that post that talks about KPIs, product-level empowerment, about focusing on growth more holistically, actually removing bottlenecks and silos, empowering teams at the product level, and instrumenting themselves to be able to actually get granular feedback.

If possible – assuming you want to spend some quality time – read that post and comment after you have read “Go corporate of go home”.

So next time, when you pitch about disruption, about the end of banks/banking, about collaboration/co-operation, or about any other technology solving world hunger, please make sure you have an answer on how to get to your new destination. I would suggest you keep forward compatibility in mind.

This is a refreshingly honest and lucid commentary–nice provocative and useful work. Note that there appears to be a small typo in the send to last paragraph, using word ‘of’ rather than ‘or’? Being of dutch ancestry, I suspect that the way one sometimes translates to the other might be the contributor here 😉